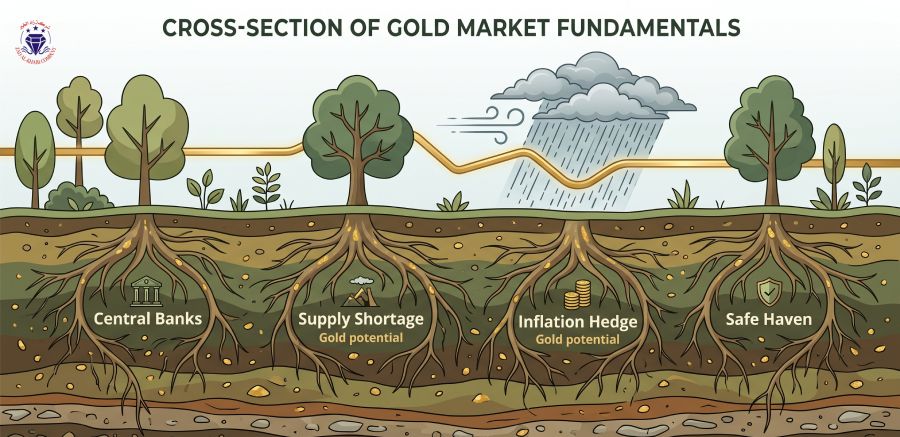

A tree does not panic in a storm. Its roots hold because they were built for exactly this. Gold at $4,710 this Monday morning, April 27, is the tree in the storm. Around it, Brent crude oil has spiked to $106 per barrel — its highest level in weeks — as Trump cancelled Pakistan peace talks and Iran reiterated it will not open Hormuz while the US Navy blockade continues. The Dollar Index jumped to 99.3. Silver is flat near $76. And gold is simply holding, not panicking, not collapsing. This is what structural support looks like from the ground.

The fundamental case for gold has not changed this week. What has changed is the noise around it. The FOMC meets Tuesday and Wednesday. Chair Powell speaks Wednesday. US Q1 GDP data lands Wednesday. All of this is short-term weather. The roots are the long-term supply and demand balance, the central bank accumulation cycle, and the slow deterioration of trust in paper currencies globally. None of those have moved.

What is genuinely new this week is J.P. Morgan’s latest research, which now forecasts the Fed may actually hike rates by 25 basis points in Q3 2027 — the first hike projection since the rate cut cycle began. This is the bank that also has a gold price target of $6,000 to $6,300 by end 2026. Those two forecasts are not contradictory — gold has historically risen during periods of rate hikes when those hikes reflect uncontrolled inflation and geopolitical instability rather than a healthy economy. Stagflation — the combination of weak growth and high inflation — is emerging as the real risk in 2026. And stagflation is historically one of gold’s strongest environments. This week’s GDP data on Wednesday April 30 will be the first clear signal of whether the US economy is decelerating under the weight of $106-per-barrel oil. If growth is slowing while inflation is rising, the roots of the gold market get even deeper.